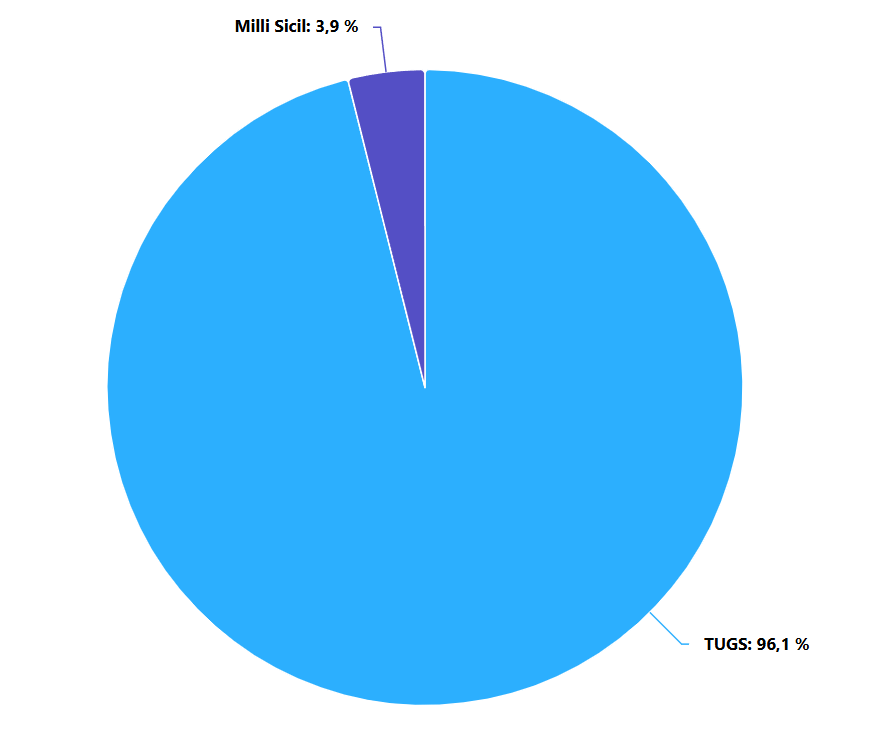

74% of R&D expenditures in Group H are “Personnel” and 3% are “Software” expenditures.

In 2020;

- 73.52% of R&D expenditures in Group H are “Personnel” (76,56 in 2019).

- 3.35% of R&D expenditures in Group H are “Software” (4.56) expenditures.

- Group H (49-51) makes 62.44% of R&D expenditures in Group H (63.26 in 2019).

- 0.60% of the total R&D expenditure of 35,623,334,563 TL made by “financial and non-financial” companies in Turkey is Group H (0.53 in 2019).

UD için AR-GE Harcama (TL)

| 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Toplam | 9.773.009 | 9.997.543 | 17.925.507 | 27.630.117 | 33.292.480 | 36.446.498 | 53.457.108 | 122.382.210 | 123.222.506 | 155.496.145 | 212.508.398 |

| Cari (49-51) | 95.832.208 | 128.703.936 | |||||||||

| Cari (52-53) | 47.236.385 | 72.907.308 | |||||||||

| Yatırım (49-51) | 2.537.765 | 3.995.953 | |||||||||

| Yatırım (52-53) | 9.889.787 | 6.901.201 | |||||||||

| Cari | 4.639.280 | 8.972.025 | 14.361.505 | 22.432.704 | 30.080.028 | 31.577.536 | 50.704.341 | 104.508.235 | 108.217.295 | 143.068.593 | 201.611.244 |

| 49-51 | 95.832.208 | 128.703.936 | |||||||||

| 52-53 | 47.236.385 | 72.907.308 | |||||||||

| Cari - Personel | 2.572.314 | 2.864.738 | 4.650.320 | 13.353.836 | 12.548.213 | 16.203.552 | 39.433.021 | 54.494.523 | 81.059.093 | 119.045.800 | 156.230.665 |

| 49-51 | 78.178.502 | 108.647.612 | |||||||||

| 52-53 | 40.867.298 | 47.583.053 | |||||||||

| Cari - Diğer Cari | 2.066.966 | 6.107.287 | 9.711.185 | 9.078.868 | 17.531.815 | 15.373.984 | 11.271.320 | 50.013.712 | 27.158.202 | 24.022.793 | 45.380.579 |

| 49-51 | 17.653.706 | 20.056.324 | |||||||||

| 52-53 | 6.369.087 | 25.324.255 | |||||||||

| Yatırım | 5.133.729 | 1.025.518 | 3.564.002 | 5.197.413 | 3.212.452 | 4.868.962 | 2.752.767 | 17.873.975 | 15.005.211 | 12.427.552 | 10.897.154 |

| 49-51 | 2.537.765 | 3.995.953 | |||||||||

| 52-53 | 9.889.787 | 6.901.201 | |||||||||

| Yatırım - Makine | 5.100.598 | 1.025.518 | 3.554.002 | 4.567.413 | 3.200.252 | 4.726.699 | 1.977.438 | 6.122.442 | 8.586.151 | 3.361.096 | 3.426.823 |

| 49-51 | 1.728.713 | 2.427.482 | |||||||||

| 52-53 | 1.632.383 | 999.341 | |||||||||

| Yatırım - Sabit tesis | 33.131 | 0 | 10.000 | 630.000 | 12.200 | 142.263 | 279.134 | 11.230.032 | 5.727.401 | 1.982.753 | 358.152 |

| 49-51 | 782.753 | 358.152 | |||||||||

| 52-53 | 1.200.000 | 0 | |||||||||

| Yatırım - Yazılım | 445.000 | 312.180 | 686.659 | 7.083.703 | 7.112.179 | ||||||

| 49-51 | 26.299 | 1.210.319 | |||||||||

| 52-53 | 7.057.404 | 5.901.860 | |||||||||

| Yatırım - Fikri Mülkiyet | 51.195 | 209.321 | 5.000 | 0 | 0 | ||||||

| 49-51 | 0 | 0 | |||||||||

| 52-53 | 0 | 0 |

Source: www.tuik.gov.tr

- Group H: Transport and Storage

- Group H (49-51): Land transport and pipeline transport; water transport; Airways transporting

- Group H (52-53): Storage and supporting activities for transport; postal and courier activities

- R&D: It is the regular, creative work done to increase the knowledge that includes the knowledge of society, culture and people and to use it in new applications.

- Current R&D Expenditures: Consists of personnel expenditures and other non-personnel current expenditures.

- Other Current R&D Expenditures: Includes materials, consumables, and equipment purchased to support R&D efforts in a given year.

- R&D Investment Expenditures: Annual gross expenditures related to fixed assets used in R&D programs. When they are made, they must be reported fully for the period and not recorded as a depreciation element. It should be subtracted from R&D expenditures, including all depreciation charges/provisions related to buildings, facilities and equipment, whether realized or based on a precedent. This approach is recommended for two reasons: If depreciation (i.e. a payment made to finance the replacement of existing assets) is included in current expenditure, adding capital expenditures causes double counting. In the government sector, no provision is normally made for the depreciation of fixed assets. Consequently, even within a country, comparisons between sectors cannot be made unless depreciation provisions are excluded, and totals for a national series cannot be compiled unless sector totals are based on a comparable basis.

- Machinery and Equipment Expenditures for R&D: Covers the main tools and equipment acquired for use in R&D research.

- Land and Building (Fixed Plant) Expenditures for R&D: Includes land acquired for R&D, for example test sites, laboratory areas and pilot facilities, and buildings constructed or purchased, including significant improvements, alterations and repairs.

- Computer Software Capitalized for R&D: This category includes the cost of computer software used in R&D activities for more than one year. This includes computer software that provides program descriptions and supporting materials for long-term license uses or for both system and application software.

- Intellectual Property Rights Expenditures for R&D: Refers to patent purchases, long-term licenses and other intellectual property rights for more than one year and used for R&D.

- Non-Financial Companies: They are institutional units dealing mainly with the production of market goods and non-financial services. Prior to the 2016 survey, it was used as the %22commercial segment%22.

- Financial Companies: Institutional units that deal specifically with financial intermediation or ancillary financial activities. Prior to the 2016 survey, it was used as the %22commercial segment%22.